Kenya’s banking sector has entered a new era with the introduction of the KESONIA (Kenya Shilling Overnight Interbank Average) as the common base rate for all variable-interest loans.

This reform, implemented under the guidance of the Central Bank of Kenya (CBK) and the Kenya Bankers Association (KBA), aims to establish a loan pricing framework that is transparent, predictable, and fair to borrowers.

But what exactly is KESONIA, how is it calculated and how does it affect the interest rate on your loan?

What is KESONIA?

KESONIA stands for the Kenya Shilling Overnight Interbank Average. It is the average interest rate at which banks lend money to each other on an overnight basis.

In simple terms:

- Banks often run short of cash at the end of a business day.

- To cover these shortfalls, they borrow from each other, usually for just one night.

- The rate at which they lend to one another changes daily depending on market conditions.

- KESONIA is the average of all these overnight lending rates across the banking system.

Why replace the old system?

Previously, banks used different internal formulas for calculating their base lending rates. This made it difficult for customers to compare loan offers across banks. Some borrowers suspected hidden costs or unfair pricing.

The Kenya Bankers Association (KBA) and the Central Bank of Kenya (CBK) introduced the Kenya Shilling Overnight Interbank Average (KESONIA) to standardize loan pricing across the banking industry. The new framework is designed to reward financial discipline by linking borrowers’ credit history to the interest rates they are charged, giving customers with good repayment records an opportunity to negotiate for better terms.

At the same time, KESONIA is meant to improve transparency in the credit market by ensuring that borrowers can easily predict how their loan rates might change, since the benchmark is tied directly to daily interbank activity rather than arbitrary adjustments. The reform also aligns Kenya with global banking standards, where interbank lending rates are widely used as reference points for loan pricing.

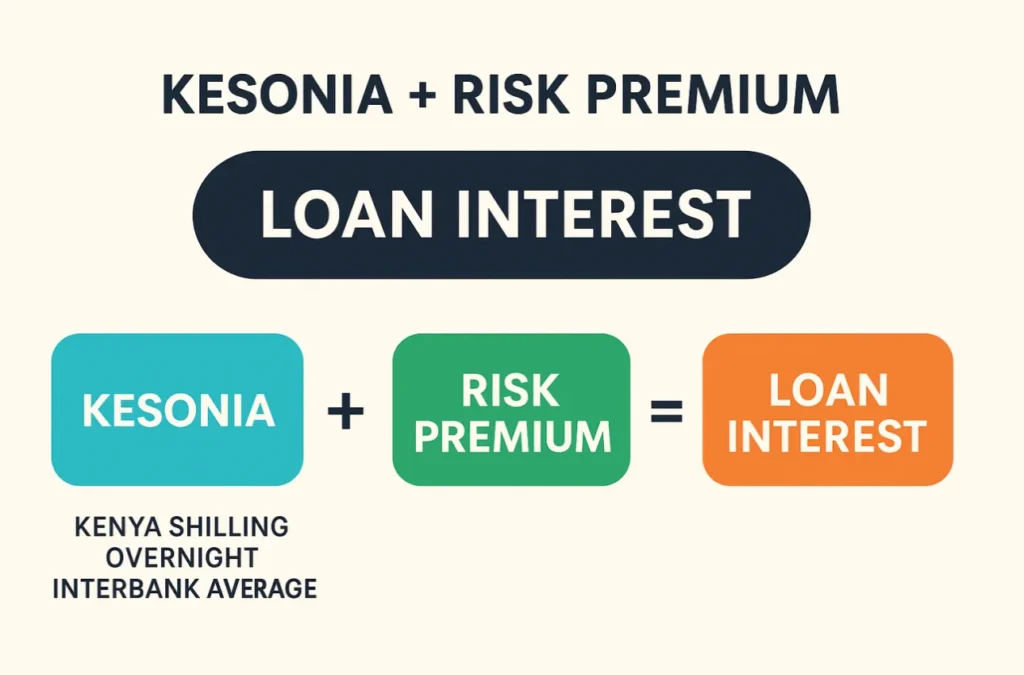

The Loan Pricing Formula

Under the new framework, the interest rate on your loan will be calculated using this formula:

Loan Interest Rate = KESONIA + Risk Premium

- KESONIA: This is the common base rate. It changes daily but is published publicly, so you know what banks are using as the starting point.

- Risk Premium: This is an extra margin added by your bank based on your creditworthiness.

- If you have a good repayment history (you pay loans on time and have not defaulted), your risk premium will be low.

- If you have a poor repayment record (missed payments, defaults, or heavy borrowing), your risk premium will be higher.

For example:

- If KESONIA today is 10% and your bank adds a 2% risk premium, your loan interest rate will be 12%.

- Another borrower with a weaker repayment history may face a 5% risk premium, giving them a loan rate of 15%.

How is KESONIA Calculated?

Kenya’s banking sector is preparing for a major shift in loan pricing following the introduction of the Kenya Shilling Overnight Interbank Average (KESONIA) as the new base lending rate. Unlike previous benchmarks, KESONIA is market-driven, reflecting actual transactions in the financial system rather than policy decisions. The rate is published daily, making it transparent for both borrowers and lenders and it adjusts automatically to reflect changes in liquidity, inflation and monetary policy.

The process of determining KESONIA is systematic. Each day, banks submit the rates at which they lent and borrowed money overnight.

The Central Bank of Kenya (CBK) compiles these figures and calculates the average, which becomes the KESONIA rate for the following day.

In an exclusive interview with News 9 Kenya, Kenya Bankers Association (KBA) Chief Executive Officer, Raimond Molenje, said the new model ensures that the base rate is firmly anchored in real market activity and not arbitrary decisions.

Molenje explained how the transition will affect borrowers.

“All existing loans will be transitioned to the new pricing framework from the time banks receive approvals of their lending models from their boards to 28th February 2026. During this transition time, banks will endeavour to ensure that all customers are not adversely disrupted in their repayment as their loans are transitioned. Banks will be able to engage customers on the components of their loan prices to ensure alignment and general awareness,” he said.

The new framework introduces more flexibility for borrowers with good repayment histories, who will have the chance to negotiate for better terms. However, customers with poor credit records are expected to face higher rates. To cushion such borrowers, KBA plans to work with stakeholders to roll out a financial literacy campaign aimed at raising awareness about the importance of maintaining a strong credit profile.

“Customers who deliberately move to improve their credit profiles will be able to receive better terms on their bank loans. This will encourage investments by customers in good credit records; thereby repairing their credit profiles,” Molenje added.

KBA also expects the framework to support financial inclusion. By using a unified base rate and allowing flexibility in the premium component, the system ensures that even borrowers with weaker credit histories are not locked out of accessing loans. Instead, they will be priced at a level that reflects their risk.

“With flexibility on the premium k, customers with poor credit scores will not be denied credit but rather access credit at a rate commensurate to their risk. This promotes financial inclusion of all segments. Besides, their inclusion at appropriate rates will also encourage customers to remedy their credit risk in order to access credit at lower interest rates. This opens them up for higher limits of loans,” Molenje further added.

The banking industry believes that, over time, the new model will encourage responsible borrowing, improve transparency in loan pricing and open the credit market to more Kenyans, particularly youth, women-led businesses and persons with disabilities.

What this means for borrowers

The new framework introduces an element of fairness by ensuring that every borrower begins with the same base rate, KESONIA. What differentiates customers is their individual risk profile, meaning those with a stronger credit history will access loans at lower rates compared to those with weaker records.

It also promotes transparency in the lending process. Since KESONIA is published daily, just like foreign exchange or stock prices, borrowers can track it in real time and understand how their loan interest rate is determined. This allows customers to see clearly how market activity feeds into the cost of their credit.

Another important feature is the incentive it creates for good financial behavior. Paying loans on time and maintaining a healthy credit score will now directly translate into lower borrowing costs, giving customers a practical reason to stay disciplined with their repayments.

However, the framework also comes with a variable nature. Because KESONIA changes daily in response to liquidity and market conditions, borrowers with variable-interest loans may see their rates fluctuate. This means that while loan costs can go down when market conditions are favorable, they may also rise during periods of tight liquidity or inflationary pressure.

{kind=link}

Discussion about this post